![]()

Methods and concepts for Value Based Management (VBM)

Financial Business Valuation

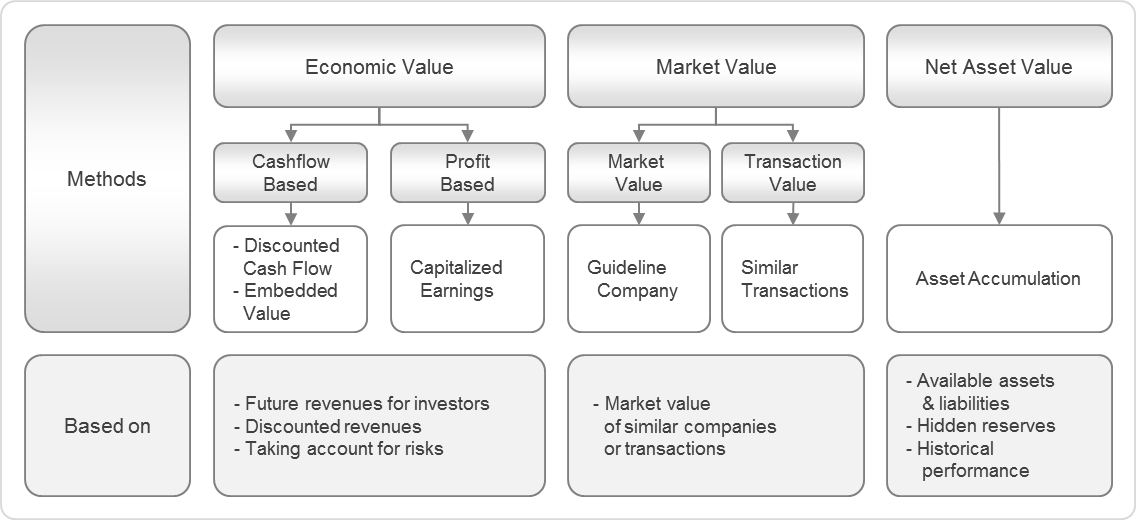

In Business Value Measurement, three different main approaches may be employed to determine its fair market value:

- the Economic Valuation Approach

- the Market Value Approach

- the Net Asset Value Approach.

While each of these approaches is initially considered in the valuation of the shareholders equity, the nature and

characteristics of the subject company and the company markets, will indicate which approach is most applicable.

Overview of the main valuation methods:

Adjusted Book Value

One of the least controversial valuation methods. It is based on the assets and liabilities of the business.

Asset Valuation

Often used for retail and manufacturing businesses because they have a lot of physical assets in inventory. Usually it is based on

inventory and improvements that have been made to the physical space used by the business. Discretionary cash from the adjusted

income statement can also be included in the valuation.

Capitalization of Income Valuation

Frequently used by service organizations because it places the greatest value on intangibles while giving no credit for physical assets.

Capitalization is defined as the Return on Investment that is expected. In a nutshell, one ranks a lists of variables with a score of 0-5

based on how strong the business is in each of those variables. The scores are averaged for a capitalization rate which is used as

multiplication factor of the discretionary income to arrive at the business' value.

Capitalized Earning Approach

Based on the rate of return in earnings that the investor expects. For no risk investments, an investor would expect For instance eight

percent.

Cash Flow Method

Based on how much of a loan one could get based on the cash flow of the business. The cash flow is adjusted for amortization,

depreciation, and equipment replacement, then the loan amount calculated with traditional loan business calculations. The amount of the

loan is the value of the business.

Cost to Create Approach (Leapfrog Start Up)

Used when the buyer wants to buy an already functioning business to save start up time and costs. The buyer estimates what it would

have cost to do the startup less what is missing in this business plus a premium for the saved time.

Debt Assumption Method

Usually gives the highest price. It is based on how much debt a business could have and still operate, using cash flow to pay the debt.

Discounted Cashflow Method

This valuation method based on free cash flow is considered a strong tool because it concentrates on cash generation potential of a business.

This valuation method uses the future free cash flow of the company (meeting all the liabilities) discounted by the firm's weighted average cost

of capital (the average cost of all the capital used in the business, including debt and equity), plus a risk factor. Since risks are not always easy

to determine precisely, the risk factor is based on historic data to measure the sensitivity of the company's cash flow, for example, through

business cycles.

Market Value Method

This valuation method is applicable for quoted companies only. The market value is determined by multiplying the quoted share price of the

company by the number of issued shares. This valuation reflects the price that the market at a point in time is prepared to pay for the shares.

This valuation method broadly takes into account the investors perceptions about the performance of the company and the managements

capabilities to deliver a return on their investments.

Asset Accumulation Method

The Asset Approach is based on the premise that it is generally possible to liquidate the property, plant and equipment (PP&E) assets of a

company, and after paying off the company's liabilities the net proceeds would accrue to the equity of the company. Valuation of assets based

on liquidity does not yield better results if the fair market value of assets is in excess of value of its assets on a liquidated basis.

Capitalized Earnings Method

The price-earnings ration (P/E) is simply the price of a company's share of common stock in the public market divided by its earnings per

share. By multiplying this P/E multiple by the net income, the value for the business could be determined. This valuation method provides a

benchmark business valuation as the non-listed companies wishing to use this method; a comparable quoted company/sector should be used.

Guideline Company Method

focuses on comparing the subject company to selected reasonably similar (or guideline) publicly-traded companies. Valuation multiples are:

derived from the operating data of selected guideline companies or evaluated and possibly adjusted based on the strengths and weaknesses

of the subject company relative to the selected guideline companies; and applied to the operating data of the subject company to arrive at an

indication of value.

Similar Transactions Method

In this method consideration is given to prices paid in recent transactions that have occurred in the subject companys industry or in related

industries.

Discounted Cashflow Method

This valuation method based on free cash flow is considered a strong tool because it concentrates on cash generation potential of a business.

This valuation method uses the future free cash flow of the company (meeting all the liabilities) discounted by the firm's weighted average cost

of capital (the average cost of all the capital used in the business, including debt and equity), plus a risk factor. Since risks are not always easy

to determine precisely, the risk factor is based on historic data to measure the sensitivity of the company's cash flow, for example, through

business cycles.

Market Value Method

This valuation method is applicable for quoted companies only. The market value is determined by multiplying the quoted share price of the

company by the number of issued shares. This valuation reflects the price that the market at a point in time is prepared to pay for the shares.

This valuation method broadly takes into account the investors perceptions about the performance of the company and the managements

capabilities to deliver a return on their investments.

Asset Accumulation Method

The Asset Approach is based on the premise that it is generally possible to liquidate the property, plant and equipment (PP&E) assets of a

company, and after paying off the company's liabilities the net proceeds would accrue to the equity of the company. Valuation of assets based

on liquidity does not yield better results if the fair market value of assets is in excess of value of its assets on a liquidated basis.

Capitalized Earnings Method

The price-earnings ration (P/E) is simply the price of a company's share of common stock in the public market divided by its earnings per

share. By multiplying this P/E multiple by the net income, the value for the business could be determined. This valuation method provides a

benchmark business valuation as the non-listed companies wishing to use this method; a comparable quoted company/sector should be used.

Guideline Company Method

focuses on comparing the subject company to selected reasonably similar (or guideline) publicly-traded companies. Valuation multiples are:

derived from the operating data of selected guideline companies or evaluated and possibly adjusted based on the strengths and weaknesses

of the subject company relative to the selected guideline companies; and applied to the operating data of the subject company to arrive at an

indication of value.

Similar Transactions Method

In this method consideration is given to prices paid in recent transactions that have occurred in the subject companys industry or in related

industries.

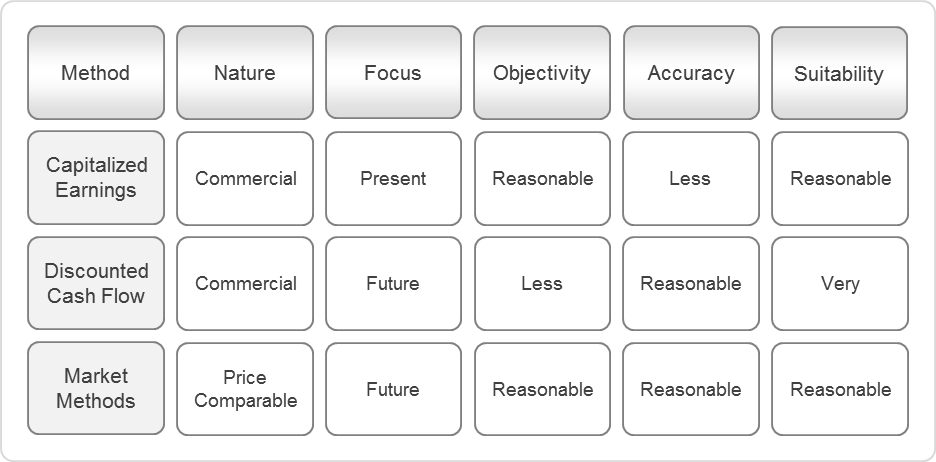

Characteristics of the main valuation methods: